The American Family Act

An Analysis of the Bennet-Brown Child Allowance

By Samuel Hammond and Robert Orr

Introduction

The American Family Act of 2019 is a legislative proposal introduced by Senator Sherrod Brown (D-OH) and Senator Michael Bennet (D-CO) to transform the Child Tax Credit into a monthly child allowance. While novel in the American context, child allowances are common across the industrialized world. Defined as any periodic, per-child cash transfer to households, child allowances come in various forms and under various names, including universal child benefits, family tax benefits, and family allowances. They are considered among the most effective tools for reducing poverty and promoting family stability, and have been endorsed and enacted by governments across the ideological spectrum.

Under the American Family Act, households would be eligible for:

$300 per month ($3,600 per year) for each child under the age of 6;

and $250 per month ($3,000 per year) for each child under the age of 17.

The benefit would begin phasing-out at a rate of 15 or 18 percent (depending on the household mix of young and older children) for individual and joint filers with incomes above $130,000 and $180,000 respectively. The maximum credit amounts are also indexed to inflation.

Relative to current law, the American Family Act would represent a substantial tax cut for all individual and joint filers with children making less than $150,000 and $200,000 respectively. The Act would also deliver much greater income support to low income families, many of whom cannot access the full benefit of CTC due to insufficient earnings. In this report, we explore the arguments for and against child allowances, and provide an analysis of the American Family Act’s distributional impact. Using the latest available survey data, we find that the American Family Act:

Creates an average net-benefit of $1,355 per family;

Reduces the number of children in poverty by 4.5 million, a 39 percent reduction;

Reduces the number of adults in poverty by 3.2 million, a 10 percent reduction;

Eliminates absolute child poverty, and reduces deep child poverty by 50 percent.

Distributional Analysis

The main tool for understanding the distributional effects of anti-poverty programs is known as the Supplemental Poverty Measure (SPM), an extension of the official poverty measure that takes into account government programs. The 2018 SPM is constructed using data from the Current Population Survey (CPS) collected in 2017, and as such does not reflect the changes to CTC introduced by the Tax Cuts and Jobs Act (TCJA).

While the TCJA doubled the maximum CTC from $1,000 to $2,000, this was largely offset by elimination of personal and dependent exemptions in higher income households. For low income households, the increase in the refundable portion of the credit was a modest $400, with the minimum earnings threshold for when the credit starts phasing-in lowered from $3,000 to $2,500. An analysis from the Center on Budget and Policy Priorities estimates that the bottom fifth of the income distribution received an average benefit of only $70 from the TCJA, and $390 in the second fifth. While non-negligible, its effect on SPM poverty is relatively small, at most moving some marginal households across the poverty line. As such, we feel confident in our estimates using a pre-TCJA baseline.

Our analysis reveals that the American Family Act would come close to cutting child poverty in half relative to poverty rates in 2017. Specifically, we find that the American Family Act would lift approximately 4.5 million children out of poverty, representing a 39 percent reduction in child poverty. Surprisingly, nearly 3.2 million adults would also be lifted out of poverty, a 10 percent reduction, reflecting the way poverty tends to concentrate in households with child dependents:

Poverty lines, including the SPM, fail to fully capture the effects of policy on low income families. A policy that substantially raises the income of someone in deep poverty may not affect the headcount poverty rate, while a policy that moves people from poverty into near-poverty will. By looking at the entire income distribution, adjusted for taxes and transfers, the progressivity of the American Family Act becomes apparent. Absolute poverty is eliminated, while the number of children in deep poverty, defined as 50% of the poverty line, is reduced by 1.8 million or 50 percent:

While low income households are the largest beneficiaries in both absolute and relative terms, the increase of the maximum per-child credit from $2,000 to $3,000-$3,600 depending on child age means virtually all middle class families benefit, as well. The average family in America would see a net benefit of $1,355. In demographic terms, Hispanic households see the largest gains, reflecting both larger family sizes and lower average incomes. Black and Asian households see the next largest gains, followed by white households, who nonetheless gain an average annual benefit of over $1,100:

Geographically, the American Family Act tends to benefit states with high rates of child poverty like California and large Hispanic communities like Texas. However, family size appears to be the biggest predictor of how much a state benefits. The state of Utah, in particular, stands out as a big winner under the American Family Act, while the District of Columbia (with its small families and high average income) benefits the least overall:

Interestingly, even though the American Family Act benefits many conservative-leaning, low density states, it also tends to benefit metropolitan areas more than non-metropolitan areas. A child allowances is thus the rare policy that binds the interests of the urban households with low-incomes, and non-urban households with large families:

How Child Allowances Reduce Poverty

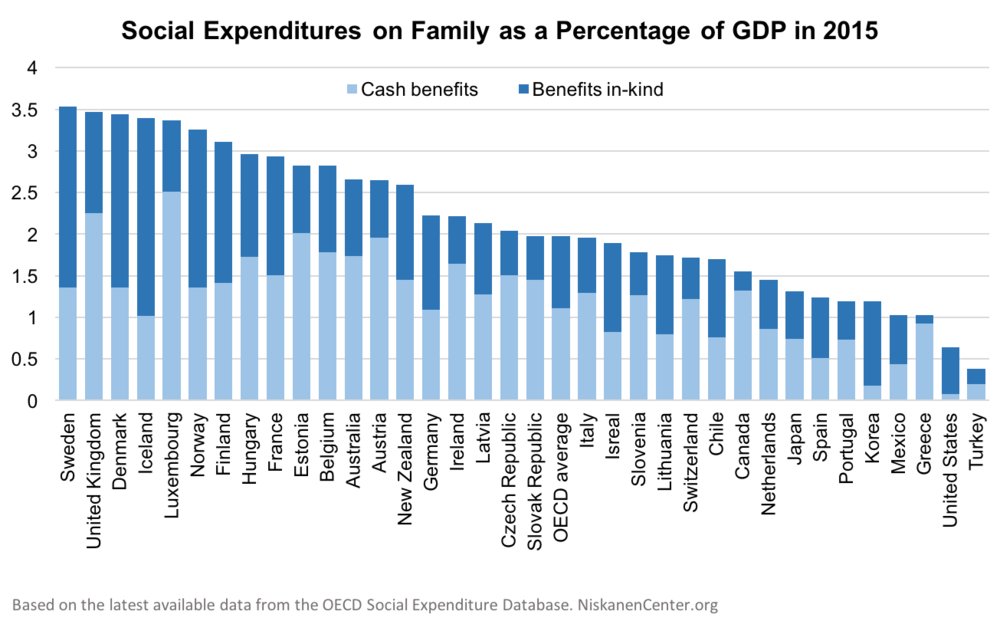

The United States has the highest rate of post-tax and transfer child poverty of any developed country. While many factors can affect poverty, a cross-national perspective reveals the reason is straightforward: Relatively small child benefits. The United States spends only 0.7 percent of GDP on family social expenditures, of which the share devoted to cash benefits, 0.1 percent of GDP, is the lowest of any OECD country. The United States would need to increase cash transfers to children and families by approximately $200 billion per year simply to match the cash benefit portion of the OECD average.

Poverty at first blush is a function of household income divided by dependents. Given two households with identical market income, the household with a dependent child will have fewer resources per-person, and therefore be more likely to fall below the poverty line. While encouraging parents to work can pull some families over the line, the laws of arithmetic mean work based anti-poverty programs can never suffice for households with children.

A new report from the National Academy of Sciences, A Roadmap to Reducing Child Poverty, reaffirms this simple truism. Citing the experience of Canada, Ireland, the United Kingdom and Australia, the report notes that countries with economies similar to the U.S. all achieve lower child poverty rates through more generous child benefits and social insurance programs oriented to households with children.

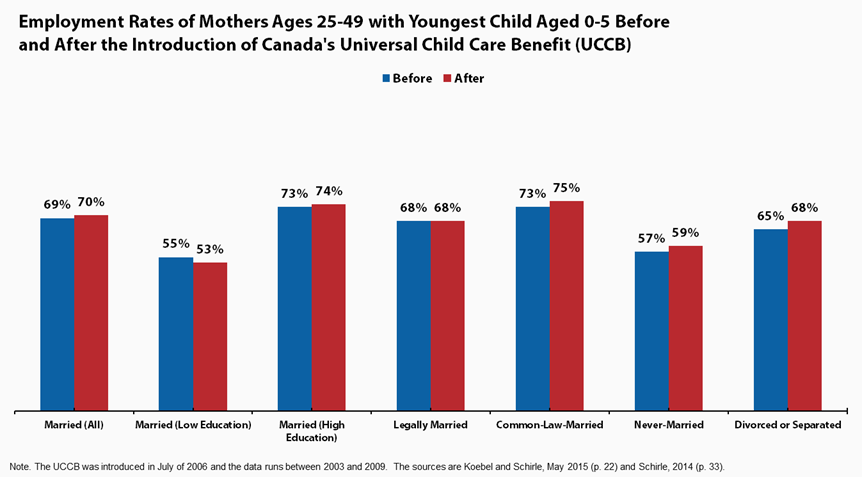

New data shows the recently expanded Canada Child Benefit cut their child poverty rate by a third in only a few short years. Structured as a child allowance, Canadian households earning less than roughly $30,000 a year are eligible to receive CAD$541.33 per month ($6,496 per year) for each child under the age of 6, and $456.75 per month ($5,481 per year) for each child aged 6 to 17. The benefit then phases out slowly for higher income families, while still reaching over 90 percent of households with children. While the benefit proposed under the American Family Act is roughly half this size, it achieves an even greater rate of poverty reduction because of America’s higher baseline rate of child poverty.

The closest analogues to a child allowance in the United States are the Child Tax Credit (CTC) and Earned Income Tax Credit (EITC). Together they represent our most powerful programs for reducing both child and adult poverty, however they currently suffer from two core limitations. First, both credits are only partially refundable, and therefore fail to reach the lowest income households. And second, both are delivered through the tax code as annual, lump-sum refunds, and therefore do not correspond to household consumption patterns. Given the EITC’s ulterior goal of promoting labor force participation, the CTC is the strongest candidate for full refundability. Similarly, as a mostly flat benefit, child allowances are comparatively simple to administer in periodic form.

It therefore makes sense for the American Family Act to build a child allowance out of the CTC. While the Social Security Administration has more experience with periodic payments, other countries, including Canada, administer child allowances through their revenue agencies. The IRS has experimented with advance payments in the past, and with additional resources there’s little reason to think it can’t match the capabilities of tax authorities in other countries.

Promoting Family Stability and Child Wellbeing

A growing academic literature has underscored the value of cash transfers on health and family stability. Consider the finding that the EITC adds a quality-adjusted life year (QALY) to the recipient at an average cost of $7,686. QALYs gained is an important measure of the effectiveness of health interventions. For comparison, Medicaid is considered cost effective at $66,000/QALY gained, which implies that expanding cash transfers through the EITC are more than eight times more cost effective as a health intervention than direct spending on low-income healthcare.

The economist Raj Chetty and his coauthors have exploited variability of tax credit generosity across states to estimate the net present value of expanding the EITC and CTC. Their central finding indicates that expanding refundable tax credits by $1,000 raises student test scores by 6-9 percent of a standard deviation, leading to higher earnings later in life that surpass the credit’s budgetary cost. These results highlight the importance of benefit fungibility. The needs of households with children are varied, from rent payments to household necessities. The neutrality of refundable credits to consumption choice allows parents to use the benefit in a way that maximizes impact given their idiosyncratic needs.

A 2015 study of expansions to Canada’s child benefit makes this clear. Previous research confirmed that its expansion led to large improvements in child outcomes, including physical and mental health, but left open the question of “how.” By studying household consumption patterns before and after the expansion, researchers found that outcomes for children improved through two distinct channels: by increasing direct expenditures on inputs like education and health (the resource channel); and by helping pay for general household items that reduced stress and improved family stability, what are known as “household stability items.” For every dollar Canada’s child benefit increased, the average household spent 13 cents more on education inputs like computers and school supplies, but also 17 cents more on rent, 8 cents more on food, and 6.5 cents more on transportation. Perhaps the most surprising result is that increases in the child benefit caused a significant drop in the consumption of tobacco and alcohol products, likely due to reduced stress.

The combination of pro-family and anti-poverty effects from child allowances are one of the reasons they are popular across the ideological spectrum. After the right-wing government in Hungary enacted large child benefits, for example, abortion rates plunged. Christian conservatives in the United States have defended child allowances on a similar basis, pointing to surveys that find 28 percent of women who have an abortion do so because of the financial stress of a child. At the same, child benefits were substantially increased by center-left parties in Britain and Canada with the primary goal of poverty alleviation. To the question of whether a child allowance is a conservative or progressive idea, the correct answer is “both.”

Addressing Objections to Child Allowances

Opponents of child allowances sometimes argue unconditional cash transfers to households with children will reduce work incentives and recreate the “poverty trap” of traditional welfare. This is based on a fundamental confusion. In the U.S. context, the 1996 welfare reform to Aid to Families With Dependent Children (AFDC) remains a strong reference point for policymakers. However, the work disincentive in AFDC was created not by cash assistance, but by the high implicit marginal tax rate on earnings as the benefit was clawed back. In some cases, a dollar earned by an AFDC recipient corresponded to a dollar reduction in benefits, creating an implied marginal tax rate of 100 percent. A child allowance that is flat for the vast majority of the income distribution does not suffer from this problem. Under the American Family Act, a dollar earned by a low income household with children is a dollar kept.

Research shows the pure “income effect” of cash transfers on work effort is small, and at low levels of income may even be positive given the relaxation of household credit and liquidity constraints. The experience of other countries bears this out. The enactment of Canada’s child allowance was essentially neutral to employment and labor force participation on net, but in way that divided along family type. Contrary to the stereotype of the “welfare queen,” the employment and labor force participation rates of single mothers increased thanks to the child allowance, as did employment rates of educated married women. Both groups used the benefit to afford child care and enter the labor market on the margin. The only group that experienced a decline in employment was married mothers with low levels of formal education, reflecting the preferences of some single earner households. There was no discernible impact on male employment.

A narrow focus on recipients can also potentially miss the bigger picture. When Canada expanded its child allowance substantially in 2016, total employment in the economy actually increased. As the Governor of the Bank of Canada noted, “the changes to the [Canada] child benefit program has been highly stimulative.” Families with young children have a higher marginal propensity to consume, implying that child benefits have a large fiscal multiplier effect. Given that Canada was still recovering from the 2008 recession, the expansion of the Canada Child Benefit helped move the country closer to full employment.

Others argue that child allowances represent redistribution from the childless to households with children and therefore oppose such programs on fairness grounds. Setting aside the qualitative difference between having children and other life style choices, this argument is misleading for two reasons. First, it neglects the fact that all adults were at one point children. Adults who grow up having benefited from a child allowance but who do not have kids of their own therefore receive the same personal benefit as adults who grow up to have large families. Second, it neglects the horizontal nature of the transfer. Unlike real estate, the returns to human capital investments in children cannot be borrowed against or sold as equity. Child allowances are a way around this problem. Given that child allowances raise the future earning potential of children, and adults reach their maximum earning potential relatively late in life, the tax system effectively stands in for a missing credit market, transferring future income to the present during a period when household budgets are particularly tight.

The final objection often levied at child benefits is their potential effect on birth rates. While there is some evidence child benefits can influence households that are on the fence about having kids achieve their ideal family size, there is no evidence for the argument that low income families have children simply to collect larger benefits. Except under an extraordinarily generous child allowance, the costs associated with raising a child remain much higher.

Conclusion

The American Family Act of 2019 would transform the existing Child Tax Credit into a true child allowance. All families would receive a sizable increase in income support for their children, with an average benefit increase of $1,355. Low income households would see the largest gains. Relative to 2017, 4.5 million children would be lifted out of poverty, representing a 39 percent decrease in child poverty. Absolute child poverty would be eliminated, and deep poverty would be cut in half. Black and Hispanic headed households, large families, and families living in metro areas would see the largest benefits.

In addition to reducing poverty, the international evidence on child allowances and research on existing refundable tax credits in the United States suggests the American Family Act would improve parent and child health, promote family stability, and raise child test scores. Together, this reflects the flexibility of child allowances to meet the diverse needs of parents and their children.